The central London office market is forecast to attract £60 billion of overseas capital over the next five years, the highest five-year total for over 20 years, according to Knight Frank’s annual London Report.

US institutional investors will be the most acquisitive in this period, with £15 billion expected to be allocated towards London office assets. Substantial volumes of capital from Germany (£6.6 billion), Greater China (£6 billion), Singapore (£5.5 billion) and South Korea (£4 billion) will also fuel record investment activity.

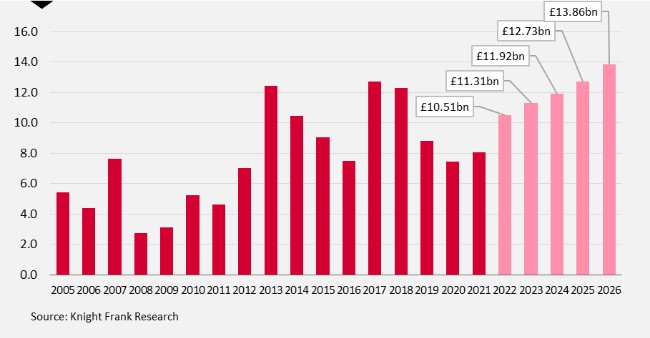

With £5.3 billion of deals currently under-offer, 2022 is expected to see £10.5bn of global capital investment into London offices, a 17% rise compared to 2021. This will be driven by pent-up demand being released as cross-border travel and social restrictions ease, as well as a broader investor base looking to deploy capital into grade-A offices with strong lease terms and sustainability credentials.

The US is expected to be the largest geographic source of capital in 2022, with £2.6 billion expected to flow into central London office assets. This will be followed by Germany (£1.1 billion), Greater China (£1.1 billion) and Singapore (£1 billion).

The forecast follows a strong 2021, which saw investment transactions for London offices hit £12.3 billion, £3 billion higher than 2020, representing the highest annual increase since 2017. During the year, international capital allocations towards the London office market also increased by £1 billion, with US investors representing £2.4 billion out of the £9 billion of foreign investment flows. There was a strong return of UK based investors accounting for £3 billion of transactions. Strong flows from UK institutions are likely to continue as the occupier market strengthens with c.25-30% of future transaction volumes.

ESG and repurposing to drive London’s Green Recovery

London’s attractive pricing compared to other cities and greater number of BREEAM-rated stock, estimated to be around 1,078 offices–more than double any other European gateway city, are key contributing factors, with investors looking to futureproof portfolios against obsolescence risks and meet stainability targets.

Knight Frank’s analysis of data looking at green ratings and office assets, found that prime central London office buildings with a BREEAM Excellent or Very Good rating enjoy a 10.5% and 10.1% premium on sales price, respectively, compared to equivalent unrated buildings. With 2021 seeing a 50% increase in central London office take up, with 8.19 million sq ft leased, and 7.5 million sq ft of current live requirements, occupier demand for best-in-class space also continues to position the city positively.

Nick Braybrook, Head of London Capital Markets at Knight Frank, commented: “The sheer volume of global capital expected to flow into the London office market over the next five years reflects the strong ESG and real estate investment fundamentals on offer. Global investors have, and will continue to, focus on the long-term picture where London’s prospects offer the returns that opportunistic capital seeks. A large weight of smart institutional money is waiting in the wings to be deployed into income generating assets, and grade-A central London offices, with its sustainability credentials and robust occupier activity, will continue to underpin investor sentiment. We are projecting a 17% increase in activity in 2022, but this is just the beginning of what we expect will be a longer-term trend of rising investment into London.”

Philip Hobley, Head of London Offices at Knight Frank, commented: “This is an exciting time for London as occupiers and investors drive a shift towards more sustainable and dynamic workplaces, where wellbeing, amenity and technology are paramount. London has a fantastic opportunity to channel unprecedented demand from international investors into the reinvention of key locations, such as the South Bank, and drive repurposing of outdated assets. London is better placed than any other city in the world to deliver a green recovery.”

Shabab Qadar, London Research Partner at Knight Frank, said: “London’s attractive pricing and above inflation income opportunities mean that global investment volumes are expected to continue increasing steadily over the next five years. With peak uncertainty around Covid-19 and Brexit now behind us, the easing of cross-border travel and improving economic outlook has coincided with a positive structural shift in the real estate allocations of long-term global investors. Given that a substantial wall of capital is competing in a market with low levels of available stock, we expect investors to increasingly seek repurposing opportunities within the secondary market, targeting the double-digit green rental and sales premium available.”

{kind=link}