-min")

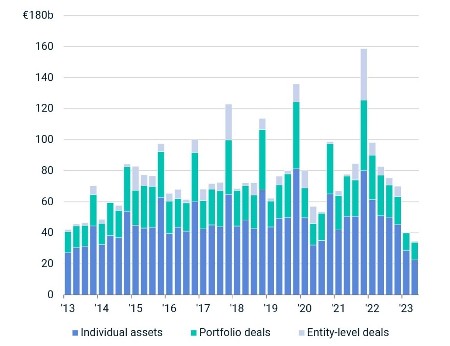

European commercial real estate investment tumbled in the second quarter, registering the lowest volume of transactions since 2010 as rising interest rates, sluggish economic growth and structural changes in office use weighed on the market, according to the latest Europe Capital Trends report from MSCI Real Assets, a part of MSCI.

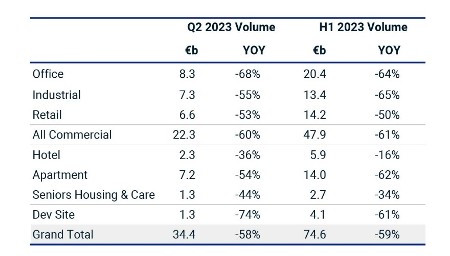

The volume of completed transactions fell 58% from a year earlier to 34.4 billion euros in April through June. The generalised slump spared no real estate sector or major national market, leaving the 74.6 billion euros of first-half property sales 59% below where volumes stood in the same period one year earlier.

Tom Leahy, Head of EMEA Real Assets Research at MSCI, said: “In these extremely challenging market conditions, the office sector stands out as hardest hit from the consequences of higher interest rates and as occupiers shift to hybrid working. There is a substantial disconnect in the pricing expectations of sellers and buyers. This will most likely continue until investors gain more visibility on borrowing costs and the health of the occupier market.”

As Europe’s largest real estate sector, offices registered the fewest number of properties sold since MSCI’s records began in 2007. Office sales totalled 8.3 billion euros in the quarter, 68% less than a year earlier. A discernible polarisation is emerging in terms of investment activity with investor demand for better quality assets holding up better than the wider market, Leahy observed.

In the industrial sector, the 7.3 billion euros of transactions was 55% below the levels of second quarter 2022, even as pricing corrected rapidly from the record low yields (capitalisation rates) of last year. Investment in the residential sector, which was also in vogue with investors when cheap debt finance was available, declined 54% to 7.2 billion euros. This was notably the case in the key northern European markets of Germany and Sweden.

Hotels were the least badly affected sector in the generalised slump, with a 16% decline in deals in the first half from a year earlier to 5.9 billion euros. This reflected the slow recovery from the impact of the COVID-19 pandemic as tourism in Spain, Portugal and other popular holiday destinations rebounded following the lifting of travel restrictions. The hotel sector’s largest transaction was Dubai Holding’s 650 million-euro purchase of the Westin Paris Vendôme in the French capital.

Paris Is Europe’s Top Investment Destination

Paris retained its position as Europe’s top investment destination as a result of the four largest real estate transactions of the first half. Overall transaction volumes were unchanged in the first six months of 2023 from a year earlier at 10.6 billion euros. Notable transactions in the second quarter were LVMH’s purchase of its Champs-Elysees store, reportedly for 770 million euros, and Valesco Group’s acquisition of Tour Sequana in the suburb of Issy-les-Moulineaux in a 460 million-euro sale-and-leaseback deal with AccorInvest.

The LVMH transaction highlighted another investment trend as owner occupiers with capital to deploy acquired their premises, converting rent liabilities into balance sheet assets. MSCI calculates that 7.5% of all office, retail, industrial and hotel transactions in the first half were owner-occupier deals. Other high profile examples include MEAG’s acquisition of a 50% share of its office in central London and French government agency AFD’s 836 million-euro forward purchase of a new headquarters in Paris.

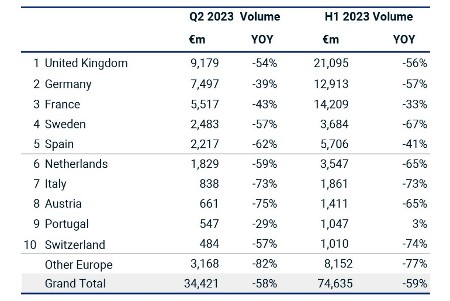

The U.K. remained Europe’s largest commercial real estate market with 21.1 billion euros of investment activity in the first half of 2023, in spite of a 56% decline from a year earlier. (MSCI’s Real Estate Market Size report, released July 24, showed the U.K. sank into fourth place behind the U.S., China and Japan respectively in 2022 in its U.S. dollar-based estimates, reflecting the correction in the value of its industrial market and the weaker British pound.)

Tom Leahy concluded: “Prospects for the remainder of the year hinge on how far central banks raise interest rates to quell persistent inflation. Once there is clarity on borrowing costs, the uncertainty over pricing should ease and deal volumes may in due course start to pick up. Asset sales by German and Swedish listed residential companies to deleverage their balance sheets highlight how, in time, owners under pressure to sell will help set a floor on valuations and pricing.”

In the U.K., the Q2 Europe Capital Trends report highlighted:

- Investment volumes fell 54% in the second quarter from a year earlier to 9.2 billion euros

- London remained in second place after Paris as the first half’s top European investment destination. The British capital recorded 7.3 billion euros of property sales, 59% lower than a year earlier during the six-month period

- Manchester ranked in sixth place among Europe’s top markets in the first half of 2023 with a 25% jump in first-half investment volumes to 1.5 billion euros. This reflected Blackstone’s purchase of Trafford Park and Heywood Distribution Park, part of a portfolio of industrial assets acquired from Harbert Management and Canmoor Asset Management

In France, the Q2 Europe Capital Trends report highlighted:

- Investment volumes declined 43% in the second quarter to 5.5 billion euros

- France remained ahead of Germany in second place and behind the U.K. in the ranking of Europe’s top national investment markets in the first half of 2023, with 14.2 billion euros of investment activity

- Five of the six largest single property transactions in Europe during the first half of 2023 were in Paris, cementing its place as the top investment destination

In Germany, the Q2 Europe Capital Trends report highlighted:

- Germany was Europe’s third-largest market after the U.K. and France in the first half with 12.9 billion euros of completed real estate transactions

- Investment volumes declined 39% in the second quarter from a year earlier to 7.5 billion euros

- The first two quarters of this year were the weakest since 2010 in terms of transaction volumes as well as the number of properties transacted

- There were only five large deals worth 200 million euros or more in the first half compared with 23 deals of that size in the same period a year earlier

- Vonovia’s 990 million-euro sale to Apollo Global Real Estate of a 30% interest in its 21,000-unit Sudewo portfolio was the European residential sector’s largest deal of the second quarter

In the Nordic markets, the Q2 Europe Capital Trends report highlighted:

- Real estate transactions plunged 75% in Nordic markets in the first half compared with a year earlier

- Sweden, the region’s largest market, ranked in fifth place after the U.K., France, Germany and Spain in the first half after a 67% decline in property sales to 3.7 billion euros

- While the struggles of Sweden’s market, notably of its listed property sector, have attracted the most attention, the Danish, Finnish and Norwegian markets all registered larger drops in investment in the first half

- Sweden slowed earlier than its regional peers and its institutions, traditionally active investors in the region, invested only 350 million euros in the first half

- Sweden’s industrial sector was the most active in the Nordic region during the first half following Blackstone’s acquisition of the 45-property portfolio from Corem

- Stockholm was Europe’s fifth biggest investment market even as transactions dropped 68% to 1.6 billion euros in the first half

In the Netherlands, the Q2 Europe Capital Trends report highlighted:

- The Netherlands slipped into sixth place behind the U.K., France, Germany, Spain and Sweden respectively in the first half after a 65% fall in first-half investment to 3.5 billion euros

- In the second quarter completed deals totalled 1.8 billion euros, 59% lower than the same quarter a year earlier

- Amsterdam ranked 12th in Europe’s top investment destinations in the first half as volumes declined 72% to 749 million euros

- Netherlands apartment investment was down by close to 50% YOY and the market remains slow post the Dutch governments reforms to the taxation system and introduction of other legislation regarding investment in residential property.

Click here to receive CRE Herald’s weekly newsletter, news alerts and insights!

{kind=link}