")

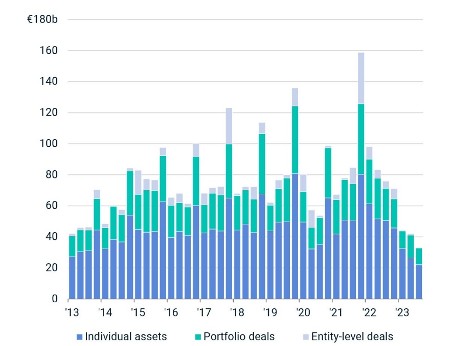

European commercial real estate registered the seventh consecutive quarter of falling investment in July through September, ensuring no market or sector had escaped the slowdown by the end of the first nine months of 2023, according to the latest Europe Capital Trends report from MSCI Real Assets.

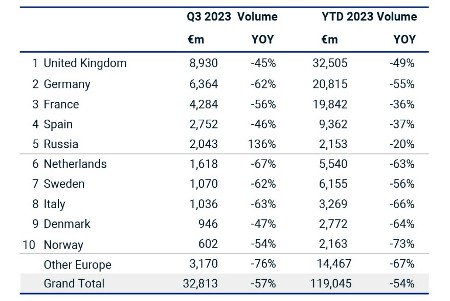

The volume of completed transactions fell 57% in the third quarter from a year earlier to 32.8 billion euros, the report showed. It was the weakest activity since 2010 and took overall investment in the first nine months of the year to 119.0 billion euros, less than half the level for the same period in 2022. Pending transactions at the start of October, typically a reliable indicator of sales in the final quarter of the year, were the lowest since 2011.

Tom Leahy, Head of EMEA Real Assets Research at MSCI, said: “The exceptionally rapid increase in interest rates meant that property went from keenly priced at the end of 2021 to overpriced by the end of 2022. Low liquidity and volatility in bond markets have complicated the price discovery process for property, causing a wide disconnect in expectations of buyers and sellers, with negative consequences for transaction activity.”

Paris remained the year’s top European investment destination as large transactions, such as luxury retailer Hermès’s 230 million-euro forward purchase of the Anjou office block from Covivio in the third quarter, limited the decline in investment volumes to 21% in the first nine months.

Pockets of Resilience

There were some areas of relative resilience amid the generalised slowdown for Europe’s commercial real estate investment market. Sales of warehouses and senior housing in the first nine months of 2023 settled around the average volumes recorded in pre-pandemic period of 2015-2019. Hotels were the least badly affected real estate sector, down 11% in the first nine months from a year earlier, following notable transactions in the French, Portuguese and Spanish markets as leisure travel rebounded.

For the office sector there was no respite, however, as the post-Covid shift to hybrid working continues to weigh on investor sentiment. The third quarter marked a record low in terms of the number of properties sold amid concerns about functional and technical obsolescence for buildings that are not best-in-class.

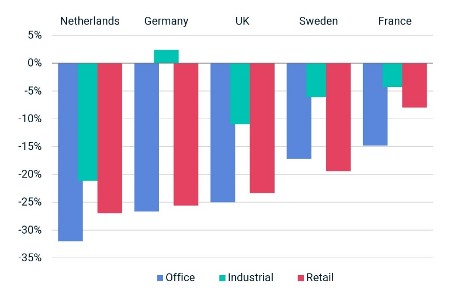

While a wide pricing expectations gap featured across all real estate sectors, the specific uncertainties weighing on the office sector amplified this mismatch in Europe’s largest markets. This differential stood at -36% in Germany’s A Cities, -28% for Central London and -22% for Paris, far worse than during 2009 at the height of the Global Financial Crisis. It underscores the extent to which would-be sellers need to reduce further reserve prices beyond the correction that has already taken place.

Transaction yields – rental income generated by a building as a proportion of the purchase price – were at a five-year high at the end of September in the major German cities and Paris, while in Central London they were back to levels last seen in 2012-2013. Office prices in the U.K. and Germany, Europe’s two largest markets, would need to fall by another 13%-15% to bring market liquidity back to its long-run average, data generated by the MSCI Price Expectations Gap model show.

The Lag in Distress Sales

Higher borrowing costs and the repricing of European real estate have already pressured some owners into divestments. Austria’s Signa Group has raised 1.8 billion euros from sales, including a retail portfolio and some of its Galeria Kaufhof properties. To reduce debt, listed residential landlord Vonovia has started to sell assets, including a 30% interest in its 21,000-unit Sudewo portfolio to Apollo for 990 million euros.

Distress to date is not widespread, though, and historical data show that there is a lag of several years between the peak of a crisis and a pick-up in the number of distress sales. It was 2012 onwards that marked the peak in distress sales post-GFC.

Tom Leahy concluded: “Distress is often what breaks the liquidity logjam by bringing price discovery, but at the moment we are still some way off from that being widespread. Germany is very much in focus as the number of properties in a distress situation has climbed to the highest in years. How this pans out will be determined by the behaviour of lenders in the months ahead.”

In the U.K., the Q3 Europe Capital Trends report highlighted:

- Investment volumes fell 45% in the third quarter from a year earlier to 8.9 billion euros. It was the second worst quarter on record for the number of properties sold. For the first nine months, deal activity fell 49% to 32.5 billion euros

- London ranked second after Paris as Europe’s top investment destination by the end of September as the number of buildings transacted fell to an all-time low. The British capital recorded 10.4 billion euros of property sales in January through September, down 57% from a year earlier

- U.K. industrial properties were one of the few European industry segments with investment volumes above the pre-Covid five-year average

- Transaction prices for warehouses in the Greater London region were 8% below their post-pandemic peak with evidence of prime assets achieving sub-4% transaction yields and in excess of asking prices

In Germany, the Q3 Europe Capital Trends report highlighted:

- Germany retained its position as Europe’s second-largest market after the U.K. by the end of September. The 20.8 billion euros of completed real estate transactions in the first nine months was 55% lower than a year earlier and the weakest activity in that period since 2010

- Investment volumes declined 62% in the third quarter from a year earlier to 6.4 billion euros

- Office transaction prices in the A Cities are down 10% from the peak reached at the end of 2021

In France, the Q3 Europe Capital Trends report highlighted:

- Investment volumes declined 56% in the third quarter from a year earlier to 4.3 billion euros

- France remained behind Germany into third place in the ranking of Europe’s top national investment markets in the first nine months of 2023, with 19.8 billion euros of investment activity. Volumes were down 36% from a year earlier

- French domiciled institutional investors slowed their acquisitions in the third quarter to the lowest since 2014

- Four of the five largest single property transactions in Europe during the first nine months of 2023 were in Paris, cementing its place as the top investment destination

In the Nordic markets, the Q3 Europe Capital Trends report highlighted:

- Sweden, the region’s largest market, ranked in fifth place in a ranking of Europe’s top real estate investment markets at the end of September after a 56% decline in property sales to 6.2 billion euros

- The Danish, Finnish and Norwegian markets all registered declines in investment volumes of at least 64% in the first nine months of 2023

- IKEA Fastigheter AB has been this year’s biggest seller of commercial real estate following its sale of 14 centres to exit Russia

- Swedish institutions, traditionally the most active investors in the region, invested only 5.5 billion euros across the region’s four countries in the first nine months. That compares with an average of 13.0 billion euros invested annually in the previous five years

- Stockholm was Europe’s fifth biggest investment market even as transactions dropped 54% to 2.7 billion euros in the year to the end of September

In the Netherlands, the Q3 Europe Capital Trends report highlighted:

- The Netherlands remained in sixth place behind the U.K., France, Germany, Spain and Sweden respectively in the year to the end of September after a 63% fall in investment to 5.5 billion euros

- In the third quarter completed deals totalled 1.6 billion euros, 67% lower than the same quarter a year earlier

- Amsterdam sank to 14th in the ranking of Europe’s top investment destinations by the end of the third quarter as volumes declined 68% to 1.2 billion euros

- The Netherlands had the widest price expectations gaps for the office, retail and industrial sectors compared with the markets of France, Germany, Sweden and the U.K.

Click here to receive CRE Herald’s weekly newsletter, news alerts and insights!

registered the seventh consecutive quarter of falling investment in July through September.){kind=link}