The volume of European commercial real estate investment transactions declined in the third quarter as the uncertain economic outlook and rising interest rates persuaded more investors to wait for greater visibility on property pricing, according to the latest Europe Capital Trends report from MSCI Real Assets, a part of MSCI.

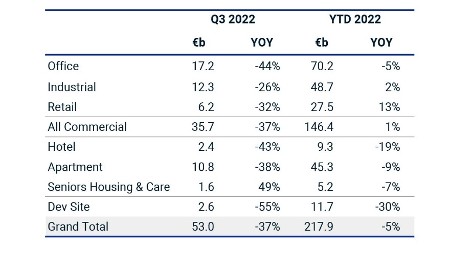

The volume of completed transactions fell 37% to 53.0 billion euros in the third quarter from a year earlier, with all the major real estate sectors and markets registering declines. The number of properties sold during the quarter was the lowest since August 2020, while the number of parties completing deals fell to a nine-year low.

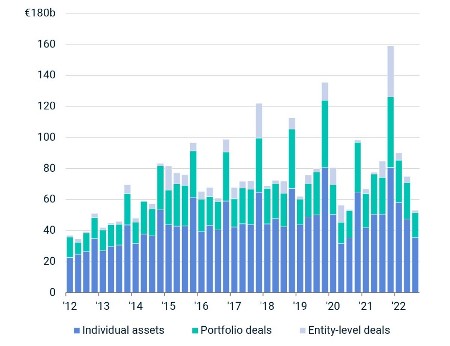

Tom Leahy, Head of EMEA Real Assets Research at MSCI, said: “We are now seeing the impact of the inflation-induced economic slowdown starting to be reflected in the real estate investment market. Price expectations are adjusting to higher borrowing costs and the prospects for rents. History tells us this recalibration will likely weigh on investment activity, as is apparent in the current slowdown and the volume of pending deals at the end of September, which was the lowest by value since 2013.”

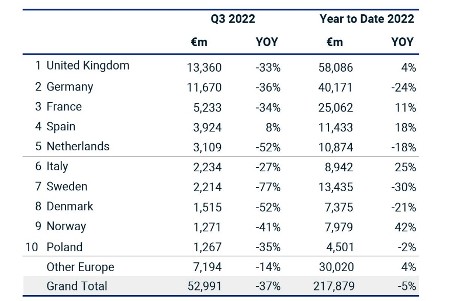

Nine of the 10 largest national markets registered declining transaction volumes during the third quarter, led by the U.K., Germany and France. The exception was fifth-placed Spain, where PGGM’s 900 million-euro purchase of a large student portfolio boosted the market’s deal flow value. Germany was the first major European market to slow this year, reflecting the anticipated economic impact of its exposure to Russian energy supplies. German transaction volumes were down 24% in the first nine months, led by the office and apartment sectors.

Europe-wide purchases of industrial, office and retail properties declined in the third quarter. Industrial assets held up best, with overall sales volumes well above the average for the preceding five years. The strength of occupier demand — evidenced by MSCI’s data showing rental growth and low vacancy rates — has supported the sector.

Data for the first nine months of 2022 show that in such an uncertain investment environment cross-border investors have favored the largest and most liquid markets. This benefitted London and Paris, which registered 17% and 11% increases in investment volumes, respectively, for this period. Another trend evident in the London office market has been the growing and sizeable price premium commanded by buildings with good environmental ratings, such as those compiled by BREEAM and LEED.

Tom Leahy concluded: “There’s a growing body of evidence of falling prices in Europe. Our UK Monthly All-Property Index in September showed the fastest fall in capital values since mid-2016. Adding to the uncertain investment environment are the pressures high interest rates are placing on borrowers refinancing mortgages.

Country highlights:

In the U.K., the Q3 Europe Capital Trends report highlighted:

- Investment volumes fell 33% in the third quarter from a year earlier to 13.4 billion euros, a two-year low led by a slowdown in office transactions

- Large deals, such as Lendlease’s purchase of 21 Moorfields in the City of London, did not prevent U.K. office transactions declining from the volumes registered in the two preceding quarters

- The U.K. is Europe’s largest commercial real estate investment market, replacing Germany in the top spot

- Investment in U.K. industrial assets remains above the five-year pre-Covid average activity levels

- Occupier demand for U.K. industrial assets remained strong, MSCI data show, with annual rental growth at a 32-year high and low vacancy rates

In Germany, the Q3 Europe Capital Trends report highlighted:

- Investment volumes declined 36% in the third quarter from a year earlier to 11.7 billion euros, led by a slowdown in apartment and office transactions, notably by domestic investors

- Germany, last year’s biggest investment market in Europe, was the first major European market to slow because of the economic impact of its exposure to Russian energy supplies. It slipped into second place behind the U.K., nine-month figures show

- Berlin, last year’s top investment destination in Europe, registered a 55% fall in investment volumes to 5.6 billion euros in the first nine months. It ranks fourth behind London, Paris and Stockholm in terms of market size

- The Berlin office market registered the weakest level of activity in the third quarter since 2013, while the A Cities office markets also registered a 50% decline compared with Q3 of 2021

In France, the Q3 Europe Capital Trends report highlighted:

- Investment volumes declined 34% in the third quarter to 5.2 billion euros

- Paris has overtaken Berlin (No. 1 in 2021) this year as Europe’s second-largest investment destination

- Investment in France’s regional office market fell to a five-year low in the third quarter

- The third quarter’s largest transaction in France was a Brookfield-led venture’s purchase of 150 avenue des Champs-Elysees in Paris, reportedly for 620 million euros

- Paris investment volumes climbed 11% in the first nine months to 13.5 billion euros

In the Netherlands, the Q3 Europe Capital Trends report highlighted:

- Investment volumes declined 52% in the third quarter to 3.1 billion euros, led by a slowdown in investment in residential properties

- Amsterdam slipped out of the top 10 investment destinations in the first nine months of 2022. The 29% decline in investment volumes to 2.6 billion euros ranks it in 13th place behind Vienna and Hamburg

In the Nordic markets, the Q3 Europe Capital Trends report highlighted:

- Sweden was Europe’s worst-performing major market in the third quarter, suffering the largest decline in investment volumes – a 77% fall to 2.2 billion euros – as domestic investors refrained from buying

- Denmark, Norway and Finland also registered declines in the third quarter but of smaller magnitudes

- Stockholm overtook Berlin to become Europe’s third-ranked investment destination during the first nine months of 2022. Activity in that period has, however, declined 28% to 5.8 billion euros

- Oslo broke into Europe’s top 10 investment destinations with record transaction volumes for the first nine months. Investment activity jumped 70% to 3.2 billion euros to rank the Norwegian capital city in ninth place behind Frankfurt and Dublin

- Helsinki more than doubled its investment activity for the first nine months with transaction volumes of 1.8 billion euros

{kind=link}