A survey of 155 leading real estate investors conducted by Knight Frank suggests the UK will reclaim its position as Europe’s leading real estate investment market in 2018, despite concerns around the terms of the country’s exit from the EU.

The survey was conducted at Knight Frank’s annual European Investment Breakfast, attended by senior professionals representing organisations with an excess of £500 billion of real estate assets under management.

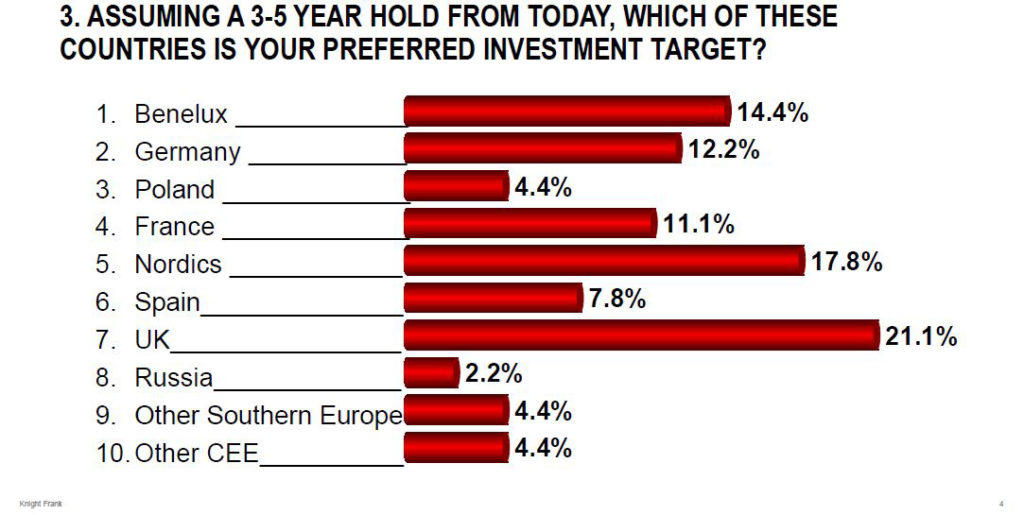

Based on a 3 – 5 year hold, 21.1% of investors identified the UK as their preferred investment market in 2018, up from 11.9% in 2017. The UK was followed by the Nordics, which was named by 17.8% of investors, and Benelux (14.4%) reflecting an increased focus on late cycle opportunities in peripheral markets. Germany, which was named by 28.5% of investors in 2017 as their primary target market, was identified by just 12.2% this year.

European buyers were the most dominant investor group in Central London in Q3 this year, accounting for nearly 40% of the market share by price, and 22% year-to-date. However, with the terms of the UK’s exit from the EU still to be determined, European investors are split on how demand for UK assets will be impacted in the mid-term.

Over half (52.5%) anticipate a reduction in investor demand over the next 3 – 5 years, with 14.6% not expecting Brexit to have any lasting impact. A third of investors see demand for UK assets increasing, reflecting a view that a positive Brexit outcome would support pricing.

With prices at historical highs in many locations, the poll suggests a shift in how investors plan to allocate capital across commercial property asset classes. For the first time, specialist assets – defined as automotive, healthcare and student accommodation – was shown to be the most attractive asset class, identified by 37% of investors as their primary target with a 3 – 5 year hold.

Dropping from the top spot as the most popular asset class, 21.7% selected industrial and distribution, down from 50% in 2017, amid concerns over pricing. Offices was named by 29.3%, with retail (7.6%) and hotels (4.3%) set to be targeted by a small minority.

European investment volumes exceed €155 billion

With 2018 mainland European investment volumes on course to exceed the ten year-average of €155 billion, investor demand is set to remain stable in 2019. A quarter (23.7%) of investors believe there will be no change, with 36.1% predicting a slight strengthening and 35.1% anticipate a slight softening in demand.

While 28.8% predicted yields may harden in 2019, the lack of liquidity in the market rather than pricing was identified as the main challenge to those wishing to place real estate capital.

Over half of those surveyed (55.3%) suggested that lack of available stock is the biggest constraint, with relatively few identifying geo-political uncertainty (15.3%) or competition from overseas investors (16.5%) as the main impediment.

Chris Bell, Managing Director, Europe, at Knight Frank, said: “While 2018 European investment volumes will be slightly down year-on-year this reflects an exceptional year in 2017 buoyed by a number of portfolio deals, rather than any softening in investor demand.

“Indeed, there is a huge weight of capital to be allocated to European real estate, including an unprecedented level of private equity dry powder, and a growing pool of private wealth. The question is where it will be deployed.

“Given pricing is at historical high levels across most markets, opportunistic investors will be looking at emerging asset classes and peripheral locations to generate returns, explaining the popularity of Benelux and the Nordics and decline in interest in Germany. In this context, the emergence of the UK as the European market of choice in 2019 is interesting, suggesting many think that pricing looks attractive.

“The survey also suggests that the growth in the industrial and distribution sector may start to slow, as investors turn their attention to specialist assets such as care homes and retirement living which are higher-yielding and supported by long-term demographic shifts.

“The challenge is liquidity, which is a legacy of the low levels of investment in 2011 and 2012. We expect increasingly levels of stock to come to market over the next 12 – 24 months, which will support investment volumes in 2019 and 2020.”

SEE ALSO : London to remain strong in commercial real estate investment despite Brexit

{kind=link}