-min")

As risks to the U.S. economy from the COVID-19 pandemic emerged in mid-March, commercial real estate lending markets began to navigate a period of price discovery, according to the latest research from CBRE.

Commercial real estate loan closings remained at high levels in Q1 2020, reflecting the strong market conditions prior to the disruption of activity towards the end of the quarter.

The CBRE Lending Momentum Index, which tracks the pace of commercial loan closings in the U.S., reached a value of 275 in March—a 4.5% increase from its Q4 2019 close and up 15% from a year ago. With the deal pipeline slowing in April, a decline in lending momentum is anticipated in Q2 2020.

READ ALSO : Commercial real estate lending activity in U.S remains strong in Q4

“Commercial mortgage markets are transitioning through a period of price discovery, with certain lenders remaining active. Interest rate floors and/or minimum spreads have become commonplace. More conservative underwriting and lower loan to values have also been instituted. Property types especially hard hit by occupancy issues or rent collections have become very difficult to finance,” said Brian Stoffers, Global President of Debt & Structured Finance for Capital Markets at CBRE.

“We expect balance sheet lenders, such as banks and life companies, along with the agencies, to continue to offer loan quotes on a selective basis. Some alternative lenders have been adversely affected by liquidity issues. The underwriting of construction and transitional loans will also remain challenging over the next few months,” added Mr. Stoffers.

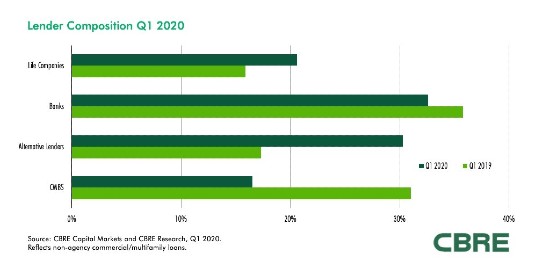

CBRE’s lender survey indicates that banks led the major non-agency lending groups in Q1 2020, accounting for 32.6% of loan closings. This share represented an increase upon a 25.1% average for H2 2019. Banks, which are better capitalized now than prior to the Global Financial Crisis (GFC), are expected to remain a source of liquidity in the coming months.

Alternative lenders (includes REITs, finance companies, debt funds) posted another strong quarter in Q1 2020, contributing 30.3% of volume. While many private equity debt funds have substantial equity to deploy, some funds are expected to struggle with liquidity issues over the near-term. The ability to underwrite value-added and construction deals may also be challenging, while opportunistic deals will increase.

Life companies were the third most active lending group in Q1 2020, accounting for 20.6% of volume—above the 15.9% share from a year ago and matching Q4 2019. While many life companies remain active in the market, they are selective in underwriting new deals.

READ ALSO : U.S commercial, multifamily mortgage loan originations decrease in Q1 2020

CMBS conduits accounted for 16.5% of lending volume in Q1 2020, down from 31% a year ago. New CMBS conduit originations were curtailed in mid-March, as market volatility caused bond spreads to widen significantly. The Federal Reserve’s recent announcement of including senior CMBS bonds as eligible collateral in its re-activated Term Asset-Backed Lending Facility (TALF) tightened bond spreads and improved the outlook for CMBS loan originations re-starting in coming months.

Underwriting on loans tracked were largely unchanged in Q1 2020, with debt service coverage ratio and underwritten cap rates matching last quarter’s results, while loan constants and the average mortgage rate were down slightly. The percentage of origination balances that pay down over the loan term fell in Q1 2020, reflecting a higher proportion of loans carrying full-term interest only. At 22.8%, this percentage was above the 17.9% average from a year ago.

“While underwriting has become more aggressive in recent years, it remains more conservative than the period leading up to the GFC, so current originations should be able withstand higher levels of stress,” added Mr. Stoffers.

{kind=link}