-min")

The Fed’s interest rate reductions, combined with continued economic growth, supported strong commercial real estate lending activity in Q4 2019, according to the latest research from CBRE.

The CBRE Lending Momentum Index, which tracks the pace of commercial loan closings in the U.S., reached a value of 263 in December 2019—virtually unchanged from its Q3 2019 close and up 4.2% from a year ago.

“A favorable capital markets environment for real estate continued to support strong commercial lending activity into year-end. Alternative lenders should remain a plentiful source of lending capital in 2020, particularly for bridge and construction loans,” said Brian Stoffers, Global President of Debt & Structured Finance for Capital Markets at CBRE.

“The multifamily agency market also posted a record year in 2019 with volume totaling $148.5 billion. The agencies will have almost $80 billion each to deploy in 2020, which should provide strong liquidity to multifamily investment,” he added.

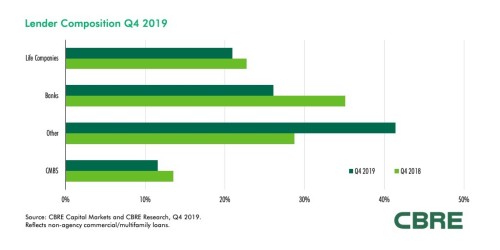

CBRE’s lender survey indicates that alternative lenders (includes REITs, finance companies, debt funds) had another strong quarter to lead origination activity in Q4 2019. Alternative lenders accounted for 41% of total non-agency volume—up from 29% in Q3 2019 and 29% a year earlier.

READ ALSO : U.S commercial real estate lending activity remains positive in Q3

Among traditional lenders, life companies accounted for 21% of non-agency lending volume in Q4 2019, down from a 29% share in Q3 2019 and from 23% a year ago. Competition for high quality life company product increased in Q4 2019, leading to the relative decline.

Banks’ share of volume rose to 26% in Q4 2019 from 24% in Q3 2019, but was down from 35% a year ago.

Among the originations tracked by CBRE, CMBS lenders accounted for 12% of total volume in Q4 2019, down from 17% in Q3 2019 and 14% in Q4 2018.

Corporate bond and CMBS pricing remained tight. Between October 2019 and late January 2020, BBB-rated corporate bond spreads tightened by close to 30 basis points (bps). Spreads on benchmark 10-year AAA-rated CMBS bonds narrowed by close to 20 bps over the same period. With tight spreads, CMBS is positioned to build on the strong issuance volume, which contributed to a new post-recession high of $97.8 billion in 2019.

Underwriting on loans tracked became more conservative in Q4 2019, marked by higher debt service coverage and lower LTV ratios. The percentage of loans carrying either partial or full interest-only terms fell to 64.1% in Q4 2019 from a high of 67.9% in Q3 2019.

Source:CBRE

{kind=link}