-min")

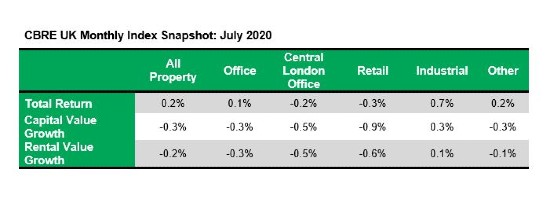

Capital values fell -0.3% across all UK Commercial property in July 2020, according to the latest CBRE Monthly Index. Over the month, rental values decreased -0.2%. July is the first month since the beginning of the Covid-19 crisis to report positive returns at 0.2% at the all property level, thanks to income return of 0.5%.

The Retail sector reported a -0.9% decline in capital values in July. Rental values declined -0.6% over the month and total returns were -0.3%. Standard Shops South East was the strongest performing Retail subsector with capital values falling -0.5%, with total returns of 0.0% – the first time returns have emerged from negative territory in any Retail subsector since February.

The Office sector posted a decrease in capital values of -0.3% over the month, slightly more than the decline posted in June (-0.2%). Rental values continued to weaken for the sector, falling -0.3% in July. Nonetheless, total returns remained positive at 0.1%. In July West End and Midtown Offices performed worse than the sector average posting capital value growth of -0.7%. Rental values also fell -0.7%, the subsector’s weakest rental value growth since July 2009.

In July the Industrial sector returned to positive capital growth after four months of declining values. The sector posted a 0.3% increase in capital values, with Industrials South East outperforming at 0.5%. This represents the first time any sector has reported increasing capital values since Covid-19 related restrictions were introduced in March. In July sector average rental values increased 0.1%. Total returns for the month were 0.7%.

‘At the all property level total returns have edged back into positive territory.‘

”Despite the continued fall in values, CBRE’s July Monthly Index has shown some promising signs. At the all property level total returns have edged back into positive territory. Capital values are increasing for Industrials and the value declines across the Retail sector continue to decelerate. On the other hand, the Office sector has not continued on the trajectory towards recovery, reporting a weaker performance than in June. Whether this is a sign of a more prolonged period of stagnation for Offices, or whether it can follow in the Industrial sector’s wake, remains to be seen,” said Toby Radcliffe, Research Analyst, CBRE.

{kind=link}