According to the latest Urban Land Institute’s (ULI) Real Estate Economic Forecast, U.S economy and real estate industry will continue to remain strong this year but economists and analysts expect moderate growth in the coming three years.

The “ULI Real Estate Economic Forecast” is a semiannual survey of economists and analysts at the nation’s leading real estate organizations. The forecast findings include both near-term and longer-term projections for a wide variety of key economic and industry indicators, ranging from employment figures to housing starts to property sector performance.

“Despite stock and bond market volatility in late 2018 and increasing global trade and growth concerns, the April 2019 ‘ULI Real Estate Economic Forecast’ is surprisingly consistent with the previous forecast conducted in October 2018,” said William Maher, head of research and strategy for LaSalle Investment Management and a survey participant. “Overall, expectations for 2019 and 2020 are flat to up, while the newly introduced 2021 forecast calls for slower growth and returns. Moderating growth in gross domestic product and jobs growth for 2019 to 2021 should lead to slower but still positive real estate demand and absorption.”

ULI survey’s key findings;

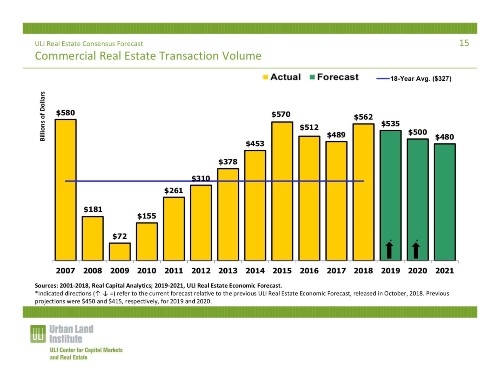

• Commercial real estate transaction volume reached $562 billion in 2018, nearing the post‐recession high of $570 billion in 2015. Annual volume is forecast to moderate during the forecast period to $535 billion in ’19, $500 billion in ‘20, and $480 billion in ‘21. Still, these are among the highest annual volumes and remain well above the long‐term average.

• Issuance of commercial mortgage‐backed securities (CMBS), a source of financing for commercial real estate, has rebounded since a low in ‘09 but to a much lower level than pre‐recession. Issuance is forecast to slightly decline throughout the forecast period at $80 billion in ‘19, $75 billion in ‘20, and $70 billion in ‘21.

• Commercial real estate prices are projected to grow at slowing rates relative to recent years, at 5.0% in ‘19, 3.7% in ’20, and 2.8% in ‘21, with the latter two years falling below the long‐term average growth rate of 4.4% for the first time since 2011.

• Institutional real estate assets are expected to provide total returns of 6.0% in ‘19, moderating to 5.0% in both ‘20 and ‘21. By property type, 2019 returns are forecast to range from industrial’s 10.3% to retail’s 2.9%. In ‘21, returns are forecast to range from industrial’s 7.0% to retail’s 3.8%.

• Commercial property rent growth is expected to continue in the next three years in all sectors, although at decelerating rates. In 2019, rent increases will range from 3.8% for industrial to 1.5% for retail. Rent increases in 2021 will range from 2.4% for industrial to 1.0% for retail. Hotel RevPAR is expected to increase by 2.5% in 2019 and by 1.0% in 2020.

• Both industrial and office vacancy rates are expected to slightly decrease in 2019 from their ‘18 rates, before edging up in both ‘20 and ‘21. Both apartment and retail availability rates are expected to see slight increases throughout the forecast period. The hotel occupancy rate is forecast to plateau in ’19, before edging down in ’20 and ‘21.

• Single family housing starts are projected to increase from their 2018 level of 870,600 units to 900,000 in ’19 which would complete eight straight years of growth, bringing annual starts to their highest level since 2007. Starts are then projected to moderate somewhat to 888,000 in ’20 and 850,000 in ‘21.

SEE ALSO : U.S office asking rents up, sales activity slows in Q1 2019, says Yardi Matrix

U.S Economy;

• The economists/analysts expect continued strong economic expansion in 2019, although at a slower rate than 2018’s post‐recession high (also reached in 2015), with further moderated growth in ‘20 and ‘21. Employment growth, expected to be strong in ’19 although lower than in the previous seven years, is projected to further slow over the following two years; still, the unemployment rate remains well below the long‐term average during the forecast period.

• GDP growth strengthened to 2.9% in 2018, up from the 2.2% growth in ‘17. Growth rates are forecast to moderate to 2.3% in ‘19 and plateau at 1.8% in ’20, and ‘21.

• Employment growth is expected to moderate from the 2.67 million jobs added in 2018 to 2.10 million jobs in ‘19, 1.42 million in ‘20, and 1.20 million in ‘21.

SEE ALSO : U.S economy grows 3.2% YoY in first quarter of 2019

• The unemployment rate is expected to continue its nine‐year decline in 2019, reaching 3.7% by the end of that year before reversing and ticking up to 3.9% in ’20 and 4.3% in ‘21.

• Compared to forecasts of 6 months ago, the forecast for GDP is less optimistic for ‘19, but more optimistic for ‘20. The unemployment rate and employment growth forecasts are both more optimistic for both ’19 and ‘20.

For more visit : ULI

{kind=link}