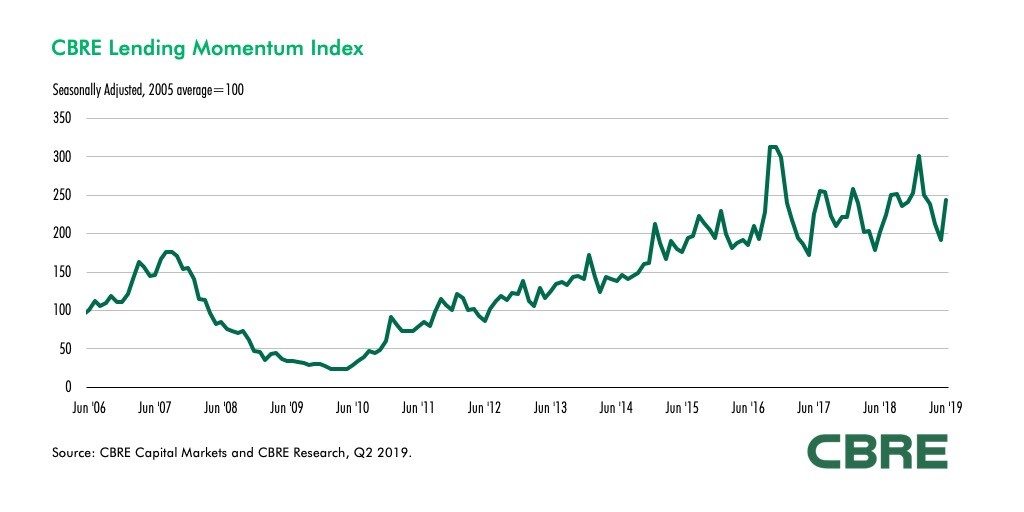

After a slow start in Q1 following market volatility at year-end, commercial real estate lending activity in the U.S gained traction in the second quarter of 2019, according to the latest research from CBRE.

The CBRE Lending Momentum Index, which tracks the pace of commercial loan closings in the U.S, closed at a value of 244 (2005 = 100) in June, up by 2.3% from March’s close. Compared with a year ago, the index is up 20.8%.

SEE ALSO : U.S commercial lending activity rises in Q4 2018

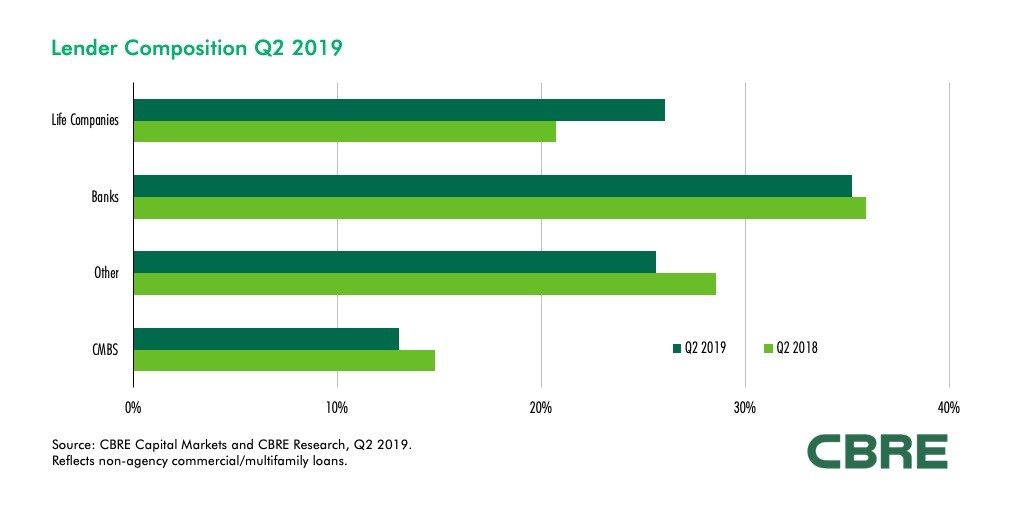

CBRE’s lender survey indicated that life company lenders had another strong quarter in Q2 2019, accounting for 26% of non-agency commercial mortgage closings—up from 21% a year ago. Banks continued to lead the four major lender categories, accounting for 35% of loan closings.

“Our survey of life company lenders indicates that all are actively quoting deals and most have robust pipelines. These lenders are quoting both fixed- and floating-rate deals, with LTVs up to 65%. Many life companies are also providing higher LTVs on select deals through higher-yielding structured loan products,” said Brian Stoffers, Global President of Debt & Structured Finance for CBRE Capital Markets.

Agency originations continue to keep pace with the market. Through May, Fannie Mae and Freddie Mac combined loan purchase volume totaled $51.8 billion versus $43 billion for the same period a year ago. With the decline in benchmark rates, mortgage rates on seven- to 10- year loans reached their lowest average since Q1 2017.

SEE ALSO : Top 10 U.S commercial/multifamily mortgage originators

Underwriting on loans tracked by CBRE Capital Markets was slightly more conservative in Q2, with increases in underwritten cap rates and debt yields. The percentage of loans carrying either partial or full interest-only terms fell below the 60% mark for the first time in nearly two years

{kind=link}